Low CIBIL Score? Get Loan in 2026

Low CIBIL Score? Here's How You Can Still Get a Loan in 2026

Aaj ke time me CIBIL score loan approval ka sabse bada factor ban gaya hai. Lekin agar aapka CIBIL score 600 se kam hai ya bilkul nahi hai, to kya aapko hamesha "No" sunna padega? Bilkul nahi. Is detailed guide me hum aapko bataenge ki kaise low CIBIL ke baavjood loan paaya jaa sakta hai — without false promises, sirf practical solutions.

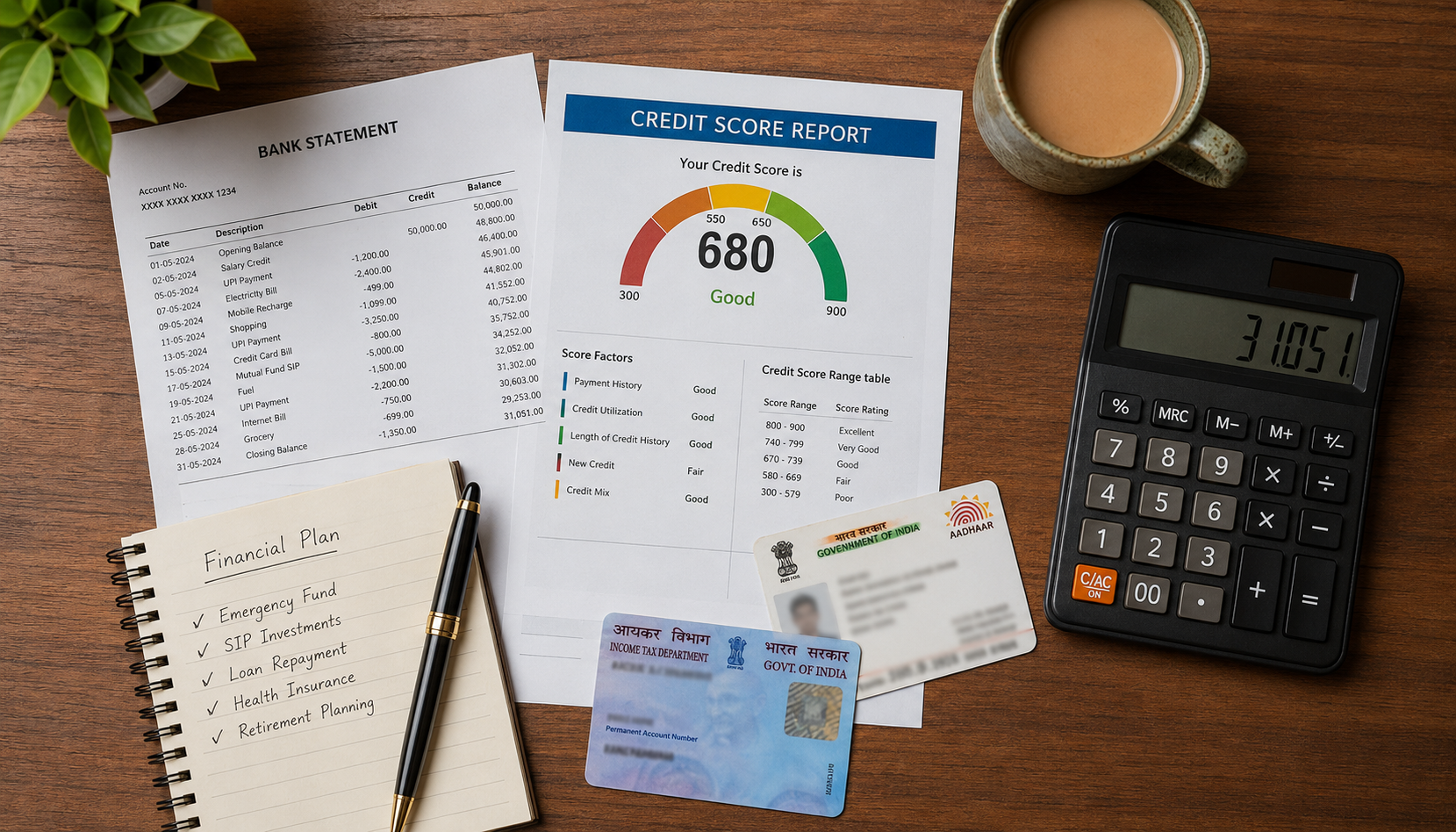

What is CIBIL Score and Why Does it Matter?

CIBIL score ek 3-digit number hota hai jo 300 se 900 tak hota hai. Ye aapki credit history ko represent karta hai — yaani aapne pehle kaise loans liye, time pe repay kiye ya nahi, credit card bills timely bhare ya late kiye, etc.

CIBIL Score Categories:

- **750 900:** Excellent — Easy approval, low interest rates

- **700 749:** Good — Approval likely, average rates

- **650 699:** Average — Approval depends, higher rates

- **550 649:** Poor — Difficult to get loan from banks

- **300 549:** Very Poor / Defaulter — Banks usually reject

Lekin yahaan ek important baat samajhne ki hai — CIBIL score sirf ek factor hai, sab kuch nahi. Lenders aapki overall financial health dekhte hain.

Why Banks Reject Low CIBIL Applications

Traditional banks aur major NBFCs automated credit scoring use karte hain. Iska matlab — agar aapka CIBIL ek certain threshold se kam hai, to file automatically reject ho jati hai, chahe aapki income kitni bhi acchi ho.

Common reasons banks reject low CIBIL applications:

- Risk Aversion: Banks ko default ka dar hota hai

- Regulatory Pressure: RBI guidelines ke under

- Automated Systems: Human review nahi hota

- One-Size-Fits-All Approach: Har profile ko same lens se dekhte hain

- No Time for Manual Underwriting: Volume zyada hota hai

7 Proven Ways to Get Loan with Low CIBIL Score

- Apply Through Loan Aggregators Like Indifunds

Loan aggregators 100+ lenders ke saath partner hote hain — including specialized NBFCs jo low CIBIL profiles ko serve karte hain. Yahan manual underwriting hoti hai, jahan aapki:

- Income stability

- Employment history

- Bank balance

- Repayment patterns

Sab kuch holistically dekha jata hai, sirf score nahi.

- Apply for Secured Loans (Loan Against Asset)

Agar aapke paas property, gold, FD, ya car hai, to secured loan apply karo. Yahaan asset collateral ban jata hai, isliye lender ka risk kam ho jata hai aur CIBIL ka impact bahut kam ho jata hai.

Options:

- Loan Against Property (LAP)

- Gold Loan

- Loan Against FD

- Loan Against Car

- Add a Co-Applicant or Guarantor

Aapke parents, spouse, ya sibling ka CIBIL agar acha hai, to unhe co-applicant banao. Lender ki nazar me risk kam ho jata hai aur approval chances badh jate hain.

Requirements for Co-Applicant:

- CIBIL score 700+

- Stable income

- Indian resident

- Age 21-65 years

- Show Strong Income Proof

Agar aapki income high aur stable hai, to kuch lenders income ke base pe loan approve kar dete hain.

What strengthens your case:

- Salary slip showing ₹50,000+/month

- Bank statement with consistent credits

- Long employment history (2+ years)

- Government/PSU job

- Working in reputed MNC

- Apply for Smaller Loan Amount

Bade loan ke liye lenders strict hote hain. Lekin ₹50,000 - ₹2 lakh ke chote loans ke liye flexibility zyada hoti hai.

Why this works:

- Lower risk for lender

- Easier to repay

- Faster approval process

- Less documentation

Once aap chota loan repay kar dete ho on time, aapka CIBIL improve hota hai aur next time bada loan mil sakta hai.

- Choose NBFC Over Banks

NBFCs (Non-Banking Financial Companies) generally more flexible hoti hain banks ke comparison me. Unka risk appetite alag hota hai aur wo low CIBIL profiles ko consider karte hain.

Top NBFCs for Low CIBIL:

- Bajaj Finserv

- Tata Capital

- Aditya Birla Capital

- Various specialized NBFCs (through aggregators like Indifunds)

- Build Credit First — Then Apply Big

Agar aap thoda time de sakte ho (3-6 months), to pehle credit improve karo then apply for major loan:

- Take a small ₹10,000 ₹50,000 loan and repay on time

- Get a secured credit card (against FD)

- Pay all existing EMIs on time

- Clear any outstanding bills

- Avoid multiple loan applications

How Indifunds Helps Low CIBIL Customers

Indifunds ek loan facilitation platform hai jo specifically low CIBIL profiles ke liye solutions design karta hai. Hum aapki application ko 100+ lender partners ke saath share karte hain, including specialized NBFCs jo bad credit profiles serve karte hain.

Indifunds Process:

- Free Eligibility Check — 2 minute me online

- Manual Underwriting — Sirf algorithm pe nahi chodte

- Multiple Lender Options — Best fit nikalte hain

- Dedicated RM Support — Har step pe guidance

- Transparent Process — Hidden charges zero

Real Customer Story

Rajesh, 34, Trader from Delhi:

"Mera CIBIL 580 tha. 3 banks ne reject kar diya tha. Indifunds ne mera case manually evaluate kiya, mera 8 saal ka business track record dekha, aur 7 din me ₹3 lakh ka loan dilwaaya. Aaj main on-time EMI bhar raha hoon aur mera CIBIL bhi improve ho raha hai."

Eligibility Criteria for Low CIBIL Loans

General Requirements:

- Indian citizen

- Age 21-60 years

- Monthly income minimum ₹25,000

- Employment/Business proof

- Valid Aadhaar + PAN

Documents Required:

- Aadhaar Card

- PAN Card

- Salary slips (last 3 months) OR

- Bank statement (last 6 months)

- Address proof

- One photograph

Interest Rates and Tenure for Low CIBIL Loans

Honest baat — low CIBIL means higher interest rates because of higher perceived risk. Typically:

- **Banks (if approved):** 12-18% p.a.

- **NBFCs:** 14-24% p.a.

- **Specialized Low CIBIL Lenders:** 18-28% p.a.

Tenure Options: 6 months to 60 months

Pro Tip: Pehle apply karo, offers compare karo, fir decide karo. Indifunds free comparison provide karta hai.

Mistakes to Avoid

- Multiple applications at same time (further damages CIBIL)

- Applying without checking eligibility first

- Hiding existing loans/debts

- Falling for "Guaranteed Approval" scams

- Paying advance fees before approval

- Ignoring loan terms and conditions

- Taking loan without repayment plan

Frequently Asked Questions

Q1. Can I get a personal loan with CIBIL score below 600?

Yes, possible hai through specialized lenders and NBFCs. Indifunds 100+ lender partners ke saath kaam karta hai, including those serving low CIBIL profiles.

Q2. Will applying for a loan further damage my CIBIL?

Sirf "hard inquiry" hone par CIBIL drop hota hai. Indifunds par eligibility check soft inquiry hota hai — yaani CIBIL affect nahi hota.

Q3. What's the minimum CIBIL score for loan approval?

Strict minimum nahi hai. Specialized lenders 500+ CIBIL pe bhi loan dete hain (based on other factors).

Q4. How long does it take to get loan with low CIBIL?

Typically 24-72 hours for approval, then 1-3 days for disbursement. Total time: 3-7 days.

Q5. Should I take loan at high interest rate?

Only if urgent need hai aur repayment capacity strong hai. Otherwise pehle CIBIL improve karne par focus karo.

Conclusion

Low CIBIL score loan paane ka end nahi hai. Sahi approach, sahi lender, aur strong income proof ke saath aap definitely loan paa sakte ho. Indifunds aise hi profiles ko serve karne ke liye design hua hai — without judgment, with full transparency.

Agar aap bhi low CIBIL ki wajah se loan se vanchit ho rahe ho, abhi free eligibility check karo Indifunds par aur dekho kya options available hain aapke liye.

Disclaimer: *Loans are subject to credit assessment and lender's discretion. Interest rates and terms may vary. T&C apply.*